ARTICLE

Changing crude oil trade flows and oil diplomacy

EU external energy policy-making is predominantly focused on natural gas, while internal energy policy-making is focused on decarbonisation and renewables. Although these might be legitimate long-term views on energy policy, they obscure the attention for short- and medium-term energy interests, where oil still plays an important role. What is the future of EU oil diplomacy?

The European Union has always played a prominent role in international oil affairs. France and the United Kingdom had an important hand in the political organisation of oil rich North Africa and the Middle East. The EU’s increasing dependency on imports from the Middle East and North Africa in the 1960s and early 1970s led to a very active oil diplomacy. The intensification in oil diplomacy efforts was further propelled by the 1973 oil crisis. This oil diplomacy became firmly embedded in the International Energy Agency (IEA), which most OECD member states joined.

Although the EU tried to engage with oil suppliers in the Euro-Arab dialogue, and in the 1990s with Russia through the Energy Charter, these efforts were quickly thwarted by objections from the United States. The EU was discouraged to pursue these more bilateral collaborations and encouraged to stick with the consumer front in the IEA.[1] From the 1970s throughout the 1990s, world oil relations have been dominated by two groups of countries, the main net-consumers of crude oil represented by the OECD/IEA countries and the main net-suppliers of oil to international markets, OPEC.

Since the turn of the century, oil flows have been changing again. The US is now a significant producer and has seen its import dependency decline substantially, while Asia has become a major importer of Middle Eastern crudes. The EU is now a mature oil market and no longer has the same political and economic significance in oil relations as before. Although the increase in US oil production has brought international oil prices down, it has also led to a new coalition in the oil market between OPEC and Russia to mitigate oversupply and low prices in the market. Before, Russia’s independent oil strategy helped to balance market power, while nowadays it is siding with OPEC for economic reasons.

© Jerry and Pat Donaho / Flickr

Drilling platform in Texas.

If this new collaboration is sustained, the strategic dependence of the EU might deteriorate without the proper policy tools to remedy the situation. EU external energy policy-making is predominantly focused on natural gas, while internal policy-making is focused on decarbonisation and renewables. Although these might be legitimate long-term views on energy policy, they obscure the attention for short and medium-term energy interests, where oil still plays an important role.

Declining importance

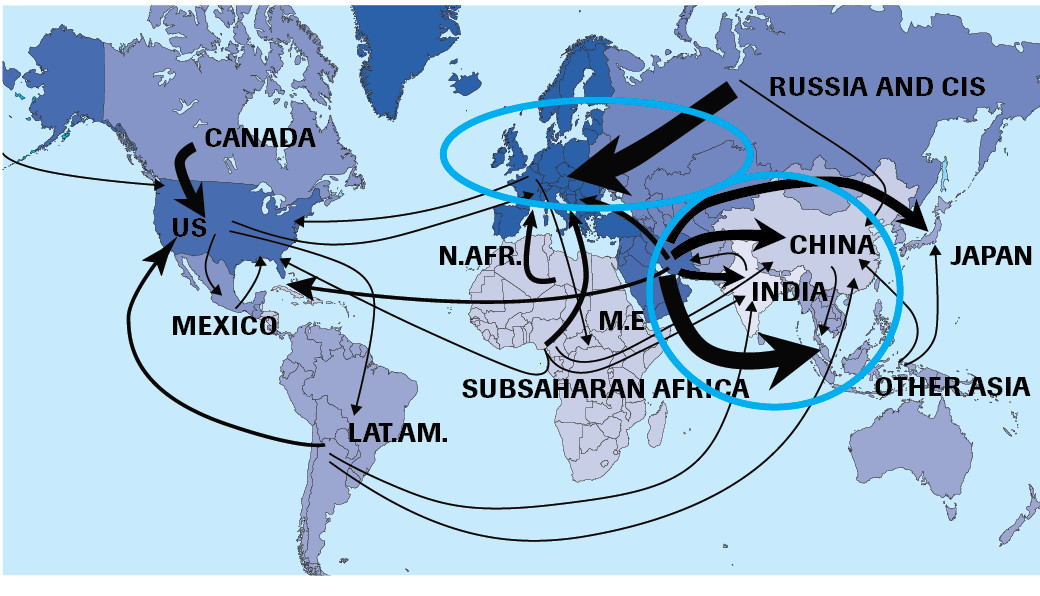

Relations between the oil consumers and producers were strained for years after 1973 and it took until the early 1990s before official talks between the two blocks could take place.[2] In 2000, the producer-consumer dialogue was institutionalised in the International Energy Forum (IEF), with – from 2003 onwards – its Secretariat in Riyadh, Saudi Arabia. The IEF did more than bringing together the IEA and OPEC member states, because from the onset other producing and consuming countries were included in the informal producer-consumer country meetings. Countries such as India and China are now, nearly twenty years later, important consuming countries, and rely heavily on supplies from the Middle East (Figure 1). They are leading members of IEF and have intense relations with oil suppliers like Saudi Arabia.

Figure 1. Oil trade flows show a large regional concentration (source: IEA, BP, Eurostat).

The intensity in the oil relations between countries in the Middle East and Asia reflects the growing importance of oil trade between these countries and the relative declining importance of oil trade with the EU and US. In the space of twenty years, the share of the OECD countries in world crude oil consumption has declined from 55% in 1998[3] to 47.9% in 2016.

Although this may seem a small change, it is, in terms of volume, significant and it reflects the increasing share of emerging markets in a growing international oil market.[4] Currently, international oil production and consumption are about 99 million Mb/d (barrels a day), compared to about 74 Mb/d in 1998.[5] Between 1998 and 2016 China’s share doubled from about 6% to 12.8% of world oil consumption, comparable to the 13.4% share of the EU; it reflects the fast growth of the Chinese energy economy in the past twenty years. China has become a substantial importer of oil and has driven growth in the international oil market in the past two decades. More mature oil markets, such as the EU, remained stable over the past twenty years. Current oil imports in the EU are, despite declining domestic production, still a little below oil imports in 2000. This decline materialised after the economic crisis of 2008 and reflects lower economic activity and efficiency gains over the period.

Shift in oil relations

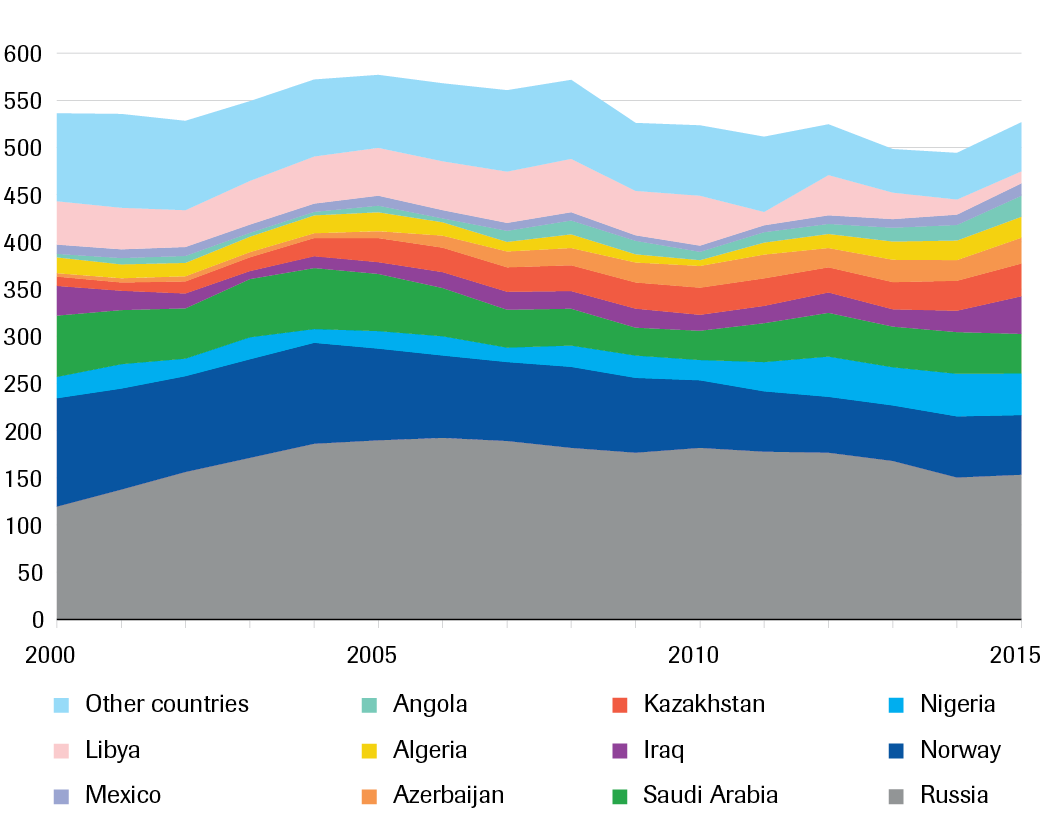

The lower oil imports of the EU in 2015 compared to 2000 could easily obscure the shift in the relative importance of EU’s main suppliers. Already in 2000 Russia was the EU’s main oil supplier (Figure 2) with a share of 22% of total oil imports; it managed to increase its share to 29% in 2015, after peak shares of 35% in 2010 and 2011. Norway nearly matched the Russian share of EU oil imports in 2000, but saw its share halved in 2015.

The political significance of this shift in relative share of oil imports is clear. Norway is a member of the European Economic Space (EES), and as such part of the EU family, while Russia is an external supplier with which relations are not always optimal. Russian oil supplies have been very reliable so far, but Russian and EU geopolitical ambitions could jeopardise this stable economic exchange. The flexibility of EU refineries to take a wide variety of crudes and oil products and the ability to blend a variety of crudes to meet the desired Brent benchmark quality reduces the strategic dependence on a certain supplier. Less flexible EU refineries or refineries connected to an oil source by pipeline, mainly in Eastern Europe, do not have this option.

© Asian Development Bank / Flickr

Oil drilling in Xinjiang, China. Between 1998 and 2016 China’s share doubled from about 6% to 12.8% of world oil consumption, comparable to the 13.4% share of the EU.

In the early 1990s, oil flows from Russia to Europe increased substantially. This was welcomed in the EU where some unease existed in relation to oil import dependence on the politically unstable Middle East. The EU’s dependence on imports from the Middle East and the disruption in flows from Kuwait and Iraq in the run up to and during the First Gulf War stimulated diversification of imports to include more Russian crude. With the increasing flow of oil available from Russia, the import dependency on suppliers from the Middle East could be reduced substantially, while the dependency on Russia increased. The energy relation with Russia, already substantial because of the gas imports, was thus intensified.

The oil relation with Russia is strategically important, and given the fact that transportation and industry will continue to rely on oil as a fuel and feedstock for quite some time, it will remain important in the future. Yet, in terms of managing the EU oil relation, very little attention is reserved for this strategically important trade relation.

© Eurostat

Figure 2. EU oil imports 2000-2015

Global oil trade has thus become much more regionally concentrated (Figure 1) in the past two decades due to changing oil demand and supply developments around the world. The focus on energy transition, the rise of new exporters and net-importing countries in the EU may have contributed to this new reality, where EU oil diplomacy makes far fewer headlines than in the decades before. This is remarkable because the share of oil in the energy mix of the EU-28 has not changed much since 1990, with a share of oil in the total primary energy mix in 2015 of 39% and in 1990 and 2000 of about 38%.

Much of the EU energy debate and diplomacy is focused on natural gas, while the share of oil in total energy demand is larger. Although the diversity of import flows appears large, the dependence on Russian imports is substantial. Moreover, the diversity of flows disguises the relative inflexibility for some EU refineries, which are optimised for certain crude blends and mask the concentration of imports from only one or two suppliers when we look at the Member State level rather than the EU level. EU statistics are therefore somewhat misleading to understand the oil relations of the EU and its Member States.

The United States: from importer to exporter

In the late 2000s, another major change in international oil markets occurred, which had a significant influence on oil flows in the world and the relative power between main oil consumers and producers. From 2009 onwards, American Light Tight Oil production (LTO) increased rapidly. Until shale gas and light tight oil became economically and technically feasible, the US was destined to become a very large oil and gas net-importing country. Oil was for this reason always an important element in its foreign policy posture, and its import dependency implied joint international oil policy interests with the EU.

The US dependence on oil imports was, however, reversed by the shale revolution. Growth of US oil production has been impressive, nearly doubling production in the space of seven years, while oil prices temporarily halted expansion of production between 2015 and mid-2016 (Figure 3). In December 2017 US oil production reached 9.9 Mb/d, breaking the previous record US production of 9.6 Mb/d of 1970.[6] The US has quickly developed into a major consumer and producer of oil. Nevertheless, the US still imports substantial volumes of oil because the its oil refinery makeup does not reflect the larger domestic availability of lighter crudes. Instead it imports heavier crudes for domestic refining and exports its excess lighter crudes. The latter became possible after the US crude oil export ban was lifted in late 2015. With the exports of light crudes, the US is in direct competition with African light oil producers. American light crudes are already competing for markets in the EU, where lighter crudes are blended with heavier ones to fit the EU refinery makeup.

© US Energy Information Administration

Figure 3. US crude oil production

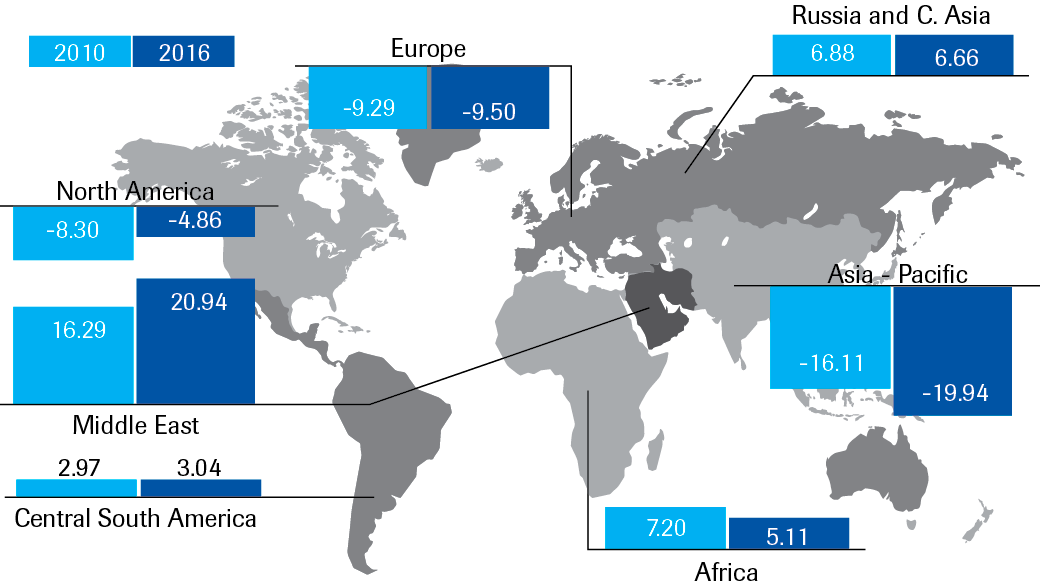

The American shale revolution has greatly influenced international oil (and natural gas) markets. Its rapid expansion contributed to world market oversupply in the period 2014-2018 and a drastic fall of oil prices in 2014. Currently, prices are recovering helped by a combination of growing world demand and OPEC-plus (Russia) production curtailments. The current expansion of American shale production, however, shows the flexibility of production and the viability of shale production at a much lower oil price level than before. Another development in the North American oil market is the steady increase of production in Canada. Oil production in Canada rose to 3.4 Mb/d in 2016. From a security of supply point of view, the North American situation has improved greatly in the past decade (Figure 4).

The improvement in the oil trade balance of North America is contrasted by the stable negative oil trade balance of the EU and the increasing deficit in Asia. The traditional shared interests in oil diplomacy of OECD/IEA countries has become less obvious, although these countries continue to share their interests in open international markets.

© ENI [2016] World Oil and Gas review

Figure 4. Crude surplus and deficit regions in the world: 2010 and 2016

EU oil (product) trade

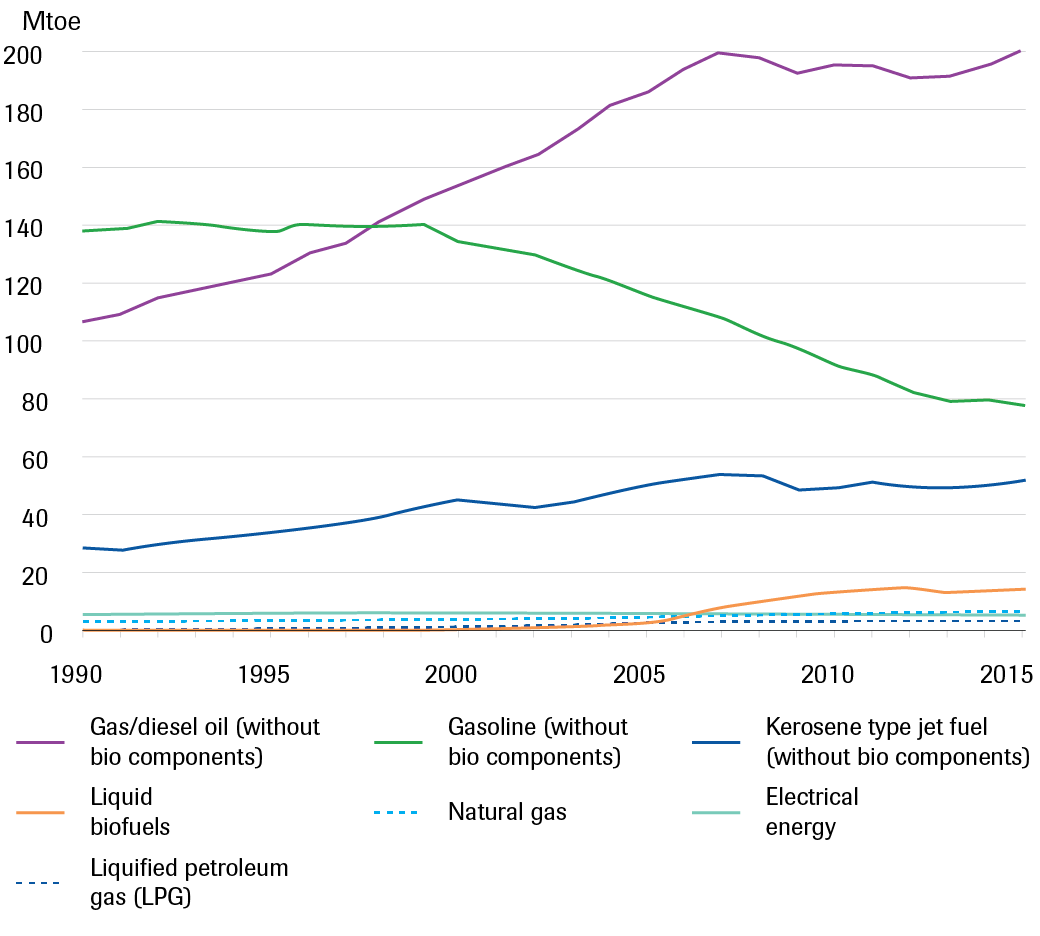

Imbalances in crude supplies and oil product demand have led to increased trade flows in certain oil products. In Europe, 47.5% of oil demand is in road transportation, while road, water and air transportation combined total about 64%.[7] A special feature of European oil product demand is the demand for diesel (in part stimulated by government policies). This is very high, compared to other markets. The increase in demand for diesel was mirrored in a gasoline demand decline (Figure 5).

Europe exports substantial volumes of gasoline to world markets and imports diesel to match oil product demand and supply

Oil product demand in the EU does not reflect the output of European refineries. Europe, therefore, exports substantial volumes of gasoline to world markets and imports diesel to match oil product demand and supply. The buildup of refining capacities in some oil producing countries, along with India and China, has contributed to a lively trade in oil products around the world. It has also led to increased competition for coastal refineries in the EU that depend on world markets in addition to their home markets.[8]

© Eurostat

Figure 5. Use of fuels in transport in the EU-28

The imbalance in oil product demand and supply in the EU can be managed through international trade flows. In the future, with more competition from electric drive trains and the blending of biofuels, the mismatch between EU oil product demand and supply could increase. Refineries will need to rely more on finding foreign markets for part of their output, while at the same time they encounter stiff competition from very large efficient export-oriented refineries in the Middle East, Russia and Asia. The traditional market for European gasoline refiners was in the US, but due to the shale revolution they are encountering more competition from US refiners. Already, refining capacity in the EU has shrunk as a result of refinery closures or refurbishments into storage facilities or bio-refineries, and this process has not yet come to an end.[9]

Conclusion

The low intensity of EU oil diplomacy is not explained by the importance of oil in the energy mix and the size of crude oil and oil product flows to Europe. With the changing posture of the US, as an important producer and consumer, and the very active oil diplomacy in Asia, the low intensity of EU oil diplomacy can perhaps be explained by several factors:

the complicated relationship with Russia, making active diplomatic efforts complex;

the belief in the speed of energy transition, where the role oil could and will play in the future is not very well understood (or ignored for the first reason);

the intensified cooperation between Russia and OPEC, which makes EU oil diplomacy not very effective and thus further encourages the EU to disengage from oil diplomacy;

the fact that security of energy supply policies are completely focused on concerns about natural gas; and

the fact that the US has traditionally encouraged the EU to deal with oil diplomacy in a multilateral setting (the IEA) and discouraged it to develop its own oil diplomacy agenda.

The EU has recently benefitted from very relaxed markets and depressed demand as a result of the economic crisis, but with the crisis declared over, and in light of a very low level of new investments in oil production in the past couple of years, the EU oil diplomacy might receive a boost when markets are expected to tighten in the early 2020s.[10] Then consumers will wonder why security of oil supply was not higher on the political agenda.