ARTICLE

Bone of contention or instrument of peace?

The role of gas in the EU’s relations with suppliers

Gas trade plays an important role in shaping the external relations of the European Union, particularly with near abroad countries in the Middle East and North Africa (MENA) and the Former Soviet Union (FSU). But does gas play a positive role in the relations between the EU and gas exporting countries? More broadly, how does gas influence Europe’s standing in the global arena? We will present two alternative views on these divisive issues in the second part of this paper. First, we will sketch the main elements of Europe’s external gas trade.

Gas trade between Europe and its suppliers – understanding current trends against the historical background

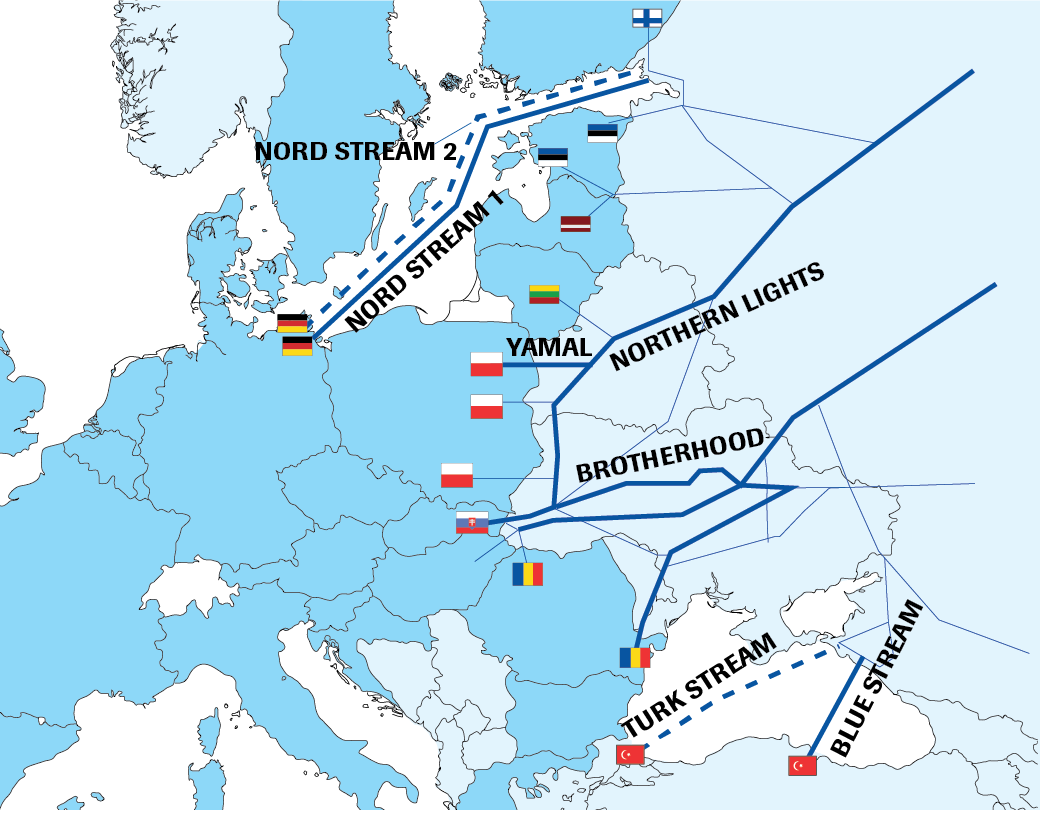

The divisiveness of debates on the role of gas is exemplified by the current polarisation of positions on Nord Stream 2 (Figure 1), Russia’s planned expansion of a pipeline that bypasses transit countries.

Figure 1. Current pipelines from Russia and pipelines under construction or planned at the EU/Turkey entry points (CIEP, 2018)

This is exposing internal divisions between European countries, between companies and politicians, and within the Brussels establishment itself. Misconceptions and simplifications abound in the debate.

The role of gas in the European energy system is a complex one, as are its macro-economic, geopolitical and societal ramifications. The following paragraphs aim to bring clarity to the debate by focussing on the international dimension of gas trade. We look at current trends against a historical background.

Europe’s gas suppliers

Somewhat ironically, the idea of importing gas from Russia is rooted in the project of distension that gained ground in the 1970s and culminated with the Helsinki Act of 1975. In spite of opposition by the United States, larger Western European countries like West Germany, France and Italy struck deals with the Soviet Union to buy substantial volumes of natural gas. In exchange, steel companies from Western Europe supplied the pipes. The tacit strategy in Western Europe was not to allow Russian gas to exceed 30 percent of consumption. This tacit rule is still respected today. The current political debate (on Nord Stream 2 and other issues) shows that it will be difficult for Russia to substantially increase its market share in Western Europe, even if Gazprom has large spare capacity.

Long-term contracts were signed in the 1970s and 1980s to underpin considerable capital investment, necessary both to develop the giant fields of Western Siberia and to build trunk lines over a distance of more than 3,000 kilometres. The legacy of these investments still has a very important bearing on EU-Russia gas relations – and arguably EU-Russia relations overall. Long-term contracts signed by State-controlled energy monopolists on both sides of the Iron Curtain and bulk investments called for demand aggregation over a number of countries and high-level political coordination. The origins of gas trade between Europe and Russia are thus essentially politically coloured.

© Gregg Westfall / Flickr

Gazprom facility across the Moscow river.

These long-term contracts, which provided the backbone of security of supply for decades, are now under threat. Since market liberalisation has allowed end-users to freely purchase gas on hubs,[1] suppliers like Gazprom had to renegotiate long-term contracts – removing one of its main features: oil indexation.[2] Up to now, this has clearly dented Gazprom’s rents.

While beneficial to European consumers in a period of oversupply, it is still unclear whether the ‘new architecture’ of gas trade[3] will benefit European consumers in the long term, as the wave of new supply wears off. Many observers highlight that long-term oil-indexed contracts provided more stability. Now, European buyers have to compete on the world stage – for instance with eager Asian buyers – to attract gas supplies. Although more transparent, hub prices can also be more volatile.

As the Soviet pipeline system was designed to serve a country that was thought to always remain united, the breakup of the USSR led to a number of unresolved issues that still define EU-Russia relations today. The most notable ones are Eastern Europe’s overreliance on Russian gas (due to the dominance of westbound connections and the scarcity of both West-East and North-South/South-North connections) and tense negotiations with Ukraine and Belarus over transit terms.

The origins of gas trade between Europe and Russia are in essence politically coloured

At the moment, Russia is strongly attempting to bypass Ukraine as a transit country by building Nord Stream 2 under the Baltic Sea and Turk Stream under the Black Sea. While supported by Germany and a number of Western oil and gas companies, the project is opposed to different degrees by the Americans – who are discussing sanctions that may block the project; the European Commission – who wants to keep Ukraine’s role as transit country for geopolitical and macro-economic reasons; and Eastern European countries – who want to preserve transit fees.

It is unclear whether Russia will be successful in building all the new pipelines that it plans, although the rationale is clear. Pipelines running through Ukraine are obsolete, and they are now used at almost full capacity. Capacity cannot be increased unless more money is invested in them, which is difficult given the current political tensions and Ukraine’s financial problems. This only leaves one option: if Russia wants to monetise its spare capacity, it needs to build new pipelines. Moreover, there is the abovementioned route diversification objective, which holds even in case Russian gas volumes would remain flat rather than grow. A likely scenario is that Russia will have to keep some transit volumes through Ukraine (although at lower levels than today), while building one or two new pipelines (although probably not before 2020).

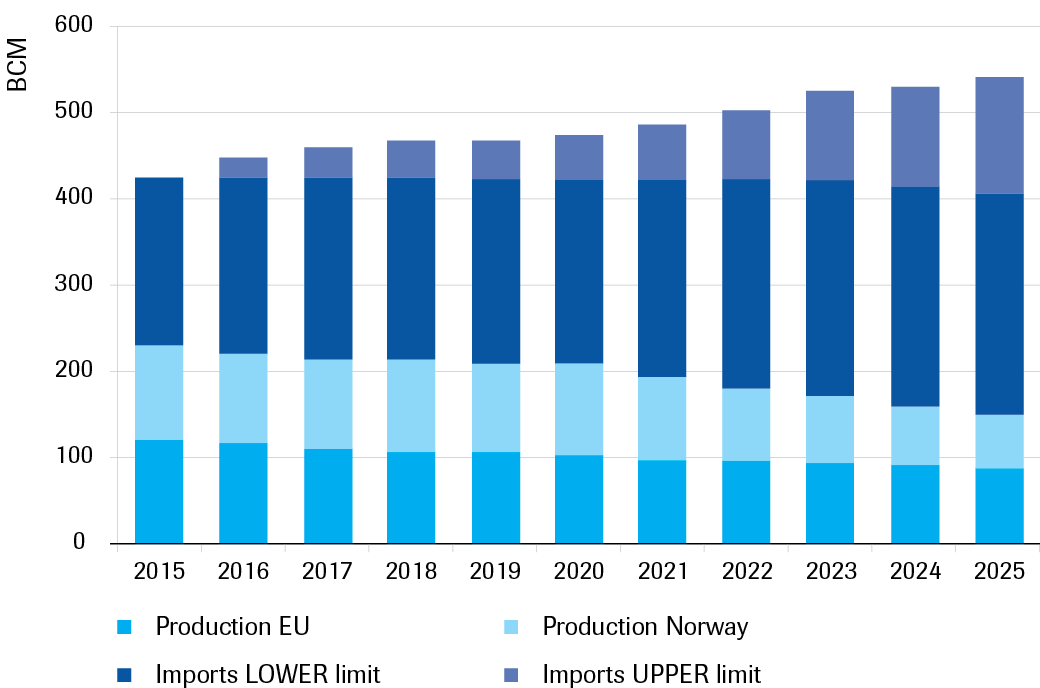

Relations between Europe and other gas suppliers are far less politicised, and the outlook for supplies from these countries looks somewhat clearer. Norway is the EU’s second gas supplier (110 Bcm), playing a particularly important role in Northwest Europe (Figure 2). Statoil – Norway’s national oil company – has accepted hub indexation before the Russians and the Algerians, managing to retain market share. Norway is recognised as a very reliable supplier in Europe. However, the EU is aware that it cannot count on Norwegian gas to fill the emerging supply-demand gap. The reason is that production rates in North Sea fields are declining and lower oil prices do not help production of gas found in association with oil.

The third supplier to the EU is Algeria (Figure 2), which primarily sells to Italy and Spain. Sonatrach, Algeria’s oil company, has tried to resist changes to gas contracts similarly to Gazprom, but eventually gave in like its Russian counterpart. In spite of a temporary spike in supplies, there is consensus that Algerian exports to Southern Europe cannot grow in the medium and long term because Algerian gas demand is rising, thus reducing the availability of export volumes.

Figure 2. Overview of domestic EU gas production and imports of gas (CIEP, BP – 2016/2017)

Apart from pipeline gas, Europe also imports 49 Bcm of Liquefied Natural Gas (LNG) (Figure 2) and this volume is expected to grow. Flexible LNG from the United States and other countries is expected to compete head-to-head with Russian gas in the years to come, bringing diversification and low prices. However, global market conditions could change between 2020 and 2025, leaving Europe to compete with high-paying Asian buyers to attract LNG cargoes.

A number of projects to boost supply diversification are on the table, namely pipelines from Iraqi Kurdistan, the East Mediterranean, Iran, Azerbaijan and Turkmenistan (Figure 3). However, they are all hampered by geopolitical tensions and financial constraints. As Europe consciously moved towards a model based on short-term rather than long-term trade, and as policies do not sketch a clear role for gas in the European energy mix, massive investments in gas pipelines are currently seen as high-risk investments. It is highly unlikely that new pipelines from these countries will be built before 2025.

In light of what has been described, what can we say about the debate on whether importing gas empowers or weakens Europe in its external relations? The two following paragraphs present alternative views: one is a pessimistic storyline, while the other is more optimistic about the role of gas.

Gas consumption and imports make Europe more vulnerable and weaken its standing in the global arena

Numerous environmentalists and investors in renewables stress that gas – a fossil fuel – contributes to global warming and delays the transition to a carbon-neutral energy system. When applied to Europe’s positioning in global affairs, this argument is associated with the conviction that Europe will benefit, also geopolitically, from being a first-mover in the energy transition.

Figure 3. Overview of existing and proposed gas infrastructure projects in Europe’s south-eastern neighbourhood (CIEP).

Additional investment in gas infrastructure is perceived as a distraction. Since the world will sooner or later fully decarbonise, it is in Europe’s interest to develop a competitive advantage in green energy technologies. This line of thought does not make a distinction between domestic and imported gas.

Sometimes, the argument that gas extraction is also locally harmful is added. Fossil fuel extraction, it is argued, creates tensions and causes detriment to local communities and to society at large, while decentralised renewables empower communities and enhance social harmony. More broadly, economic activities with less concentrated rents are seen as more prone to innovation and more compatible with the liberal-democratic model. This is a spin-off of theories that associate fossil fuel endowments with authoritarian regimes, conflicts, rent-seeking, corruption and macro-economic distortions.

Other stakeholders, not specifically concerned about environmental or societal ramifications, emphasise the security threat inherent to being dependent on foreign gas imports. In principle, they do not object to the consumption of domestically produced gas. Since European gas production is inexorably declining, however, this remains a theoretical distinction in the current debate. Even if the outlook for future European gas consumption is quite uncertain, falling domestic gas production will most likely entail higher import needs in the next 10 to 20 years (Figure 4).

Hostility to gas motivated by ecological considerations and opposition grounded on security considerations are often de facto bundled together

This narrative – increasingly widespread among policy-makers, analysts of international security and the military establishment – has gained traction in the wake of the latest Ukraine crisis due to Europe’s dependence on gas imports from Russia, a country that is increasingly perceived as hostile. This stance can simply be the basis of arguments in favour of geographic diversification, but sometimes leads to a generalised rejection of gas as a source of energy. Eastern European Member States like Poland and the Baltic Republics are particularly keen on embracing this hard security narrative.

It is important to highlight that, although conceptually distinguished, hostility to gas motivated by ecological considerations and opposition grounded on security considerations are often de facto bundled together.

© CIEP

Figure 4. Projections of EU’s and Norway’s gas production vs. EU’s import needs, based on different demand scenarios (CIEP).

Far from being a security threat, gas is a key component of Europe’s energy system and should be given a role in the transition towards clean energy

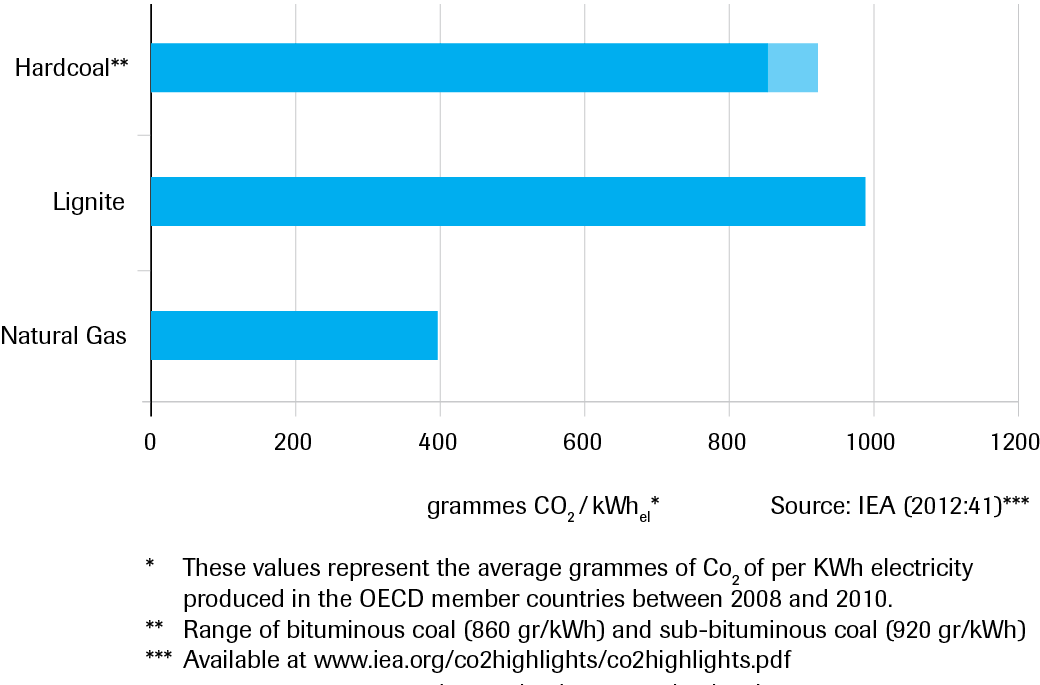

On the other hand, it could be argued that the ‘blue fuel’ – which emits 50 percent less CO2 than coal when burnt for power generation (Figure 5) – is a climate-friendly source of energy that is also compatible with the needs of European economies and energy systems, as it is more reliable than clean-yet-intermittent wind and solar.

Figure 5. Comparison of CO2 emissions of gas and different types of coal when burnt in power generation (CIEP).

It is sometimes forgotten that a number of economic activities, like heavy industry, are still very much molecule-based and their electrification is not easily attainable.[4]

Though necessary in the long term, an abrupt and full transition to renewables would be costly and destabilising for Europe. In spite of extraordinary cost savings achieved in installed capacity, the cost of adapting the whole energy system to new sources of intermittent energy is very high – and the transition needs to be carefully managed to avoid shocks to the economy and the emergence of new vulnerabilities. The opportunity cost of not picking low-hanging fruits like gas should thus be taken into account in this discussion.

The gas industry tries – albeit not always successfully – to present itself as a climate-friendly player. For instance, European gas producers – unlike their American counterparts – strongly back the introduction of more aggressive carbon pricing.[5] For them, the ideal CO2 price would be one that drives out polluting coal from electricity production and allows gas to play its role as the preferred partner to renewables. Carbon pricing reforms could still take place in Europe and this is a field of decision-making that should be watched for.

In spite of resurgent tensions, Russia has historically been a reliable gas supplier

The pro-gas camp has a number of arguments to counter the perception that gas imports make Europe vulnerable. First of all, natural gas is abundant worldwide. Only a fraction of the world’s reserves has been exploited, and technological innovations mean that more of these reserves are becoming accessible. A wave of investments in the last decade has created a situation of oversupply in the global market, which is a clear advantage for importers like the EU.

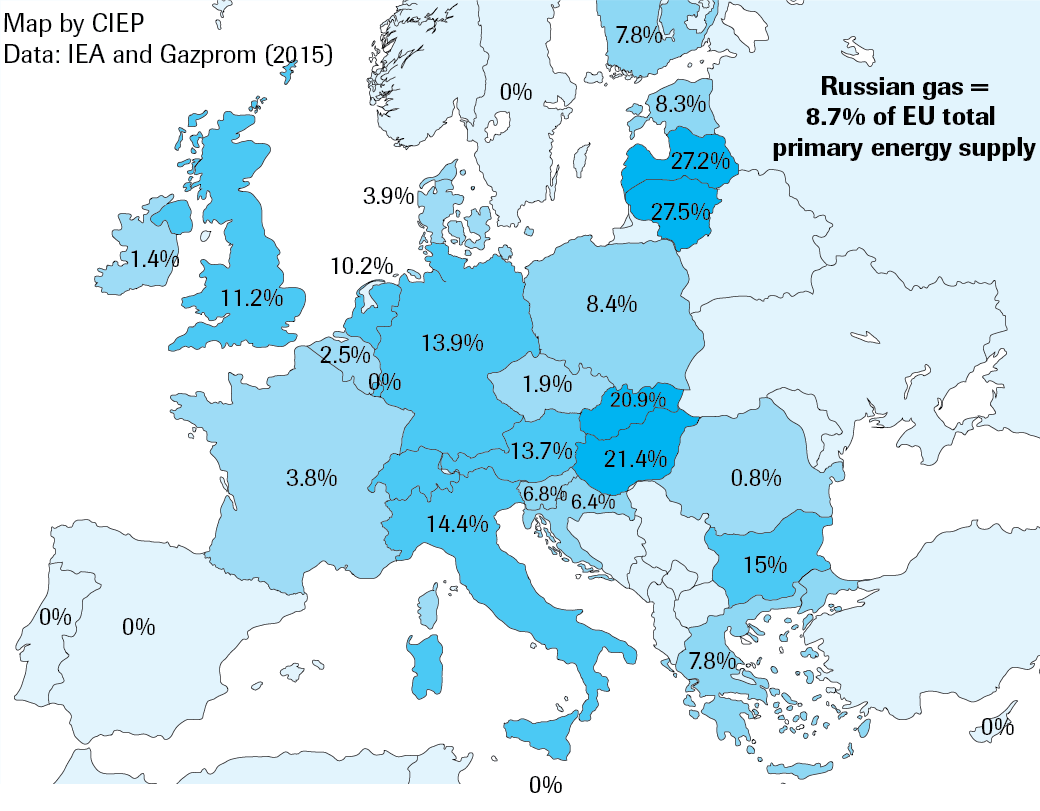

Figure 6. Share of Russian gas on total primary energy supply in the EU-28 (CIEP, IEA, Gazprom – 2015).

Besides, the advent of LNG contributes to reducing the politicisation of gas trade by stimulating competition and breaking up natural monopolies. A liquid, easily traded commodity is less vulnerable to the exertion of market power and price manipulation, which can be seen as benefitting importers. Finally, countries that are politically close to the EU (the United States, Australia and Canada) feature among the fastest-growing LNG exporters. US cargoes have already reached European shores in 2017 and Eastern European countries are particularly keen on using American LNG to diversify from Russian gas.

Moreover, preoccupations about Europe’s overreliance on Russia appear exaggerated. As a matter of fact, the EU’s dependence on Russian gas is actually only 8.7 percent when calculated in terms of primary energy consumption (Figure 6).

Although not agreed on by all the actors with a positive attitude towards gas, there is the additional argument that in spite of resurgent tensions, Russia has historically been a reliable gas supplier. After all, the only disruptions to Russian gas supply were recorded in 2006 and 2009 in relation to Ukraine transit: a few weeks of commotion over 40 years of trade relations.

© Harald Hoyer / WikimediaCommons

Pipes in Germany 2011, intended for a natural gas pipeline between Russia and Germany.

Liberal observers typically add that trade helps with cementing good political relations, and that economic interdependence acts as a deterrent to escalations. From this perspective, discontinuing gas imports from Russia or other countries would deteriorate, rather than ameliorate, Europe’s security.

Indeed, one of the lines of tension between Europe and gas suppliers is that Europe signals it needs more gas in the medium term because of its declining gas production, while it simultaneously signals it intends to get rid of all fossil fuels in the longer term. It is very hard for suppliers to allocate investments (and make macro-economic decisions) when signals are so conflicting.

Conclusion

All in all, what has been said points to the fact that Europe will keep on trading with its traditional pipeline gas suppliers for at least another two decades. Even if the breakup of the Soviet Union left a legacy of unresolved issues that still define EU-Russia energy relations, there have been promising developments such as Gazprom’s acceptance of new terms of trade.[6] Russian gas exports to the EU are expected to remain large, although for political reasons Russia will not be allowed to sell all of its spare capacity. LNG will be Gazprom’s main competitor for some time, but uncertainty reigns after 2025.

It is thus in Europe’s interest to cultivate good relationships with historical gas suppliers while simultaneously looking for new ones. However, both the use of political channels to cultivate existing relations and the aim to actively promote supply diversification have been complicated by market liberalisation – which gave power to markets clawing it back from policy-makers. Contradicting signals about the desired role for gas in the energy transition render it difficult for investors to make decisions and add uncertainty to relations between Europe and external suppliers, whose economic prosperity often depends on gas exports. If not managed carefully and gradually, this could compound instability in the neighbourhood (and particularly in the MENA and FSU regions) and represent a new line of tension in relations.