Three scenarios for globalisation in a post-COVID-19 world

The era of globalisation, open borders and global value chains is under severe pressure. Populism, protectionism and climate change have all challenged economic globalisation. The COVID-19 pandemic presents the latest challenge. This raises the question whether the outbreak of COVID-19 has sounded the death knell for economic globalisation. Three scenarios could help us grasp the potential long-term impact of the pandemic.

International trade increased rapidly after 1990, fuelled by the growth of a complex network of global value chains (GVCs). These chains represent the process of ever-finer specialisation and geographic fragmentation of production. International trade and the integration of developing countries into the world economy caused poverty to fall sharply.

In recent years, this model of economic growth based on economic globalisation has been challenged. Long before COVID-19, environmental groups, labour unions and populists all criticised free trade and globalisation for different reasons.

In 2016, tens of thousands of European citizens took the streets to protest a free trade deal being negotiated between the EU and the US. Subsequently, the negotiations on the so-called Transatlantic Trade and Investment Partnership (TTIP) stalled and have since not been resumed.

Pressure on globalisation furthermore rose as protectionist measures increased worldwide. The World Trade Organisation (WTO) estimated that the stockpile of import restrictive measures has increased since 2009 and that it affects 7,5% of world imports today. Between October 2018 and 2019, the WTO recorded 102 new trade-restrictive measures, covering USD 746,9 billion of trade flows.

The trade war between the US and China has shaken the foundations of global trade. The superpower rivalry led to a process of economic ‘decoupling’, forcing many American and Chinese companies to shift supply chains elsewhere.

The US Commerce Department has, for example, added Chinese companies such as Huawei Technologies Co LTD and ZTE Corp to its so-called ‘entity list’ – a blacklist banning US companies from supplying the two Chinese telecom giants without US government approval.

COVID-19 pandemic the death knell for globalisation?

As free trade and globalisation are increasingly under pressure, it is questionable whether economic globalisation as we know it will survive yet another punch. COVID-19 is bringing economic globalisation to the brink of collapse and could fundamentally change the way international supply chains are managed.

Bruno Le Maire, the French Minister of the Economy and Finance, views the pandemic as a "game-changer" for globalisation. According to Le Maire, the outbreak reveals an "irresponsible and unreasonable" reliance on Chinese suppliers and exposes the vulnerability of complex international supply chains.

Short-term versus long-term impact of the pandemic

In the short-term, it is highly likely that the COVID-19 pandemic will lead to a period of economic recession. The Dutch Bureau for Economic Policy Analysis (CBP) was amongst the first national agencies to officially adapt its economic outlook. On 26 March, the agency reported that an economic recession is “unavoidable”, with GDP declining between 1,2% to 7,7% in 2020.

A short period of economic recession seems unavoidable, but the question is whether COVID-19 will structurally transform globalisation on the long-term

While it seems unavoidable that we will enter a period of economic recession in the short-term, we do not know what the impact will be on the long-term. Therefore, the question is whether COVID-19 will structurally transform globalisation or we will get back to business as usual once the pandemic is over.

How to analyse the pandemic’s effect on globalisation?

To analyse the long-term effect of COVID-19 on economic globalisation, we must decompose the various elements of globalisation. Economic globalisation includes a variety of elements such as cross-border trade flows, capital flows, data flows, exchanges of people and so forth. This article will focus on the impact on global supply chains.

We can distinguish between local value chain participation, regional value chain (RVC) participation and global value chain (GVC) participation. Generally speaking, the higher the participation in intra-regional RVCs, the higher the degree of regional economic integration. Likewise, the higher the degree of participation in inter-regional GVCs, the higher the degree of economic integration into the global economy.

Assessing the level of economic globalisation by GVC participation does not fully resemble the complex reality, as various other drivers of globalisation such as people-to-people exchanges are excluded. Nevertheless, the concept of participation in GVCs helps better grasp the potential impact of COVID-19.

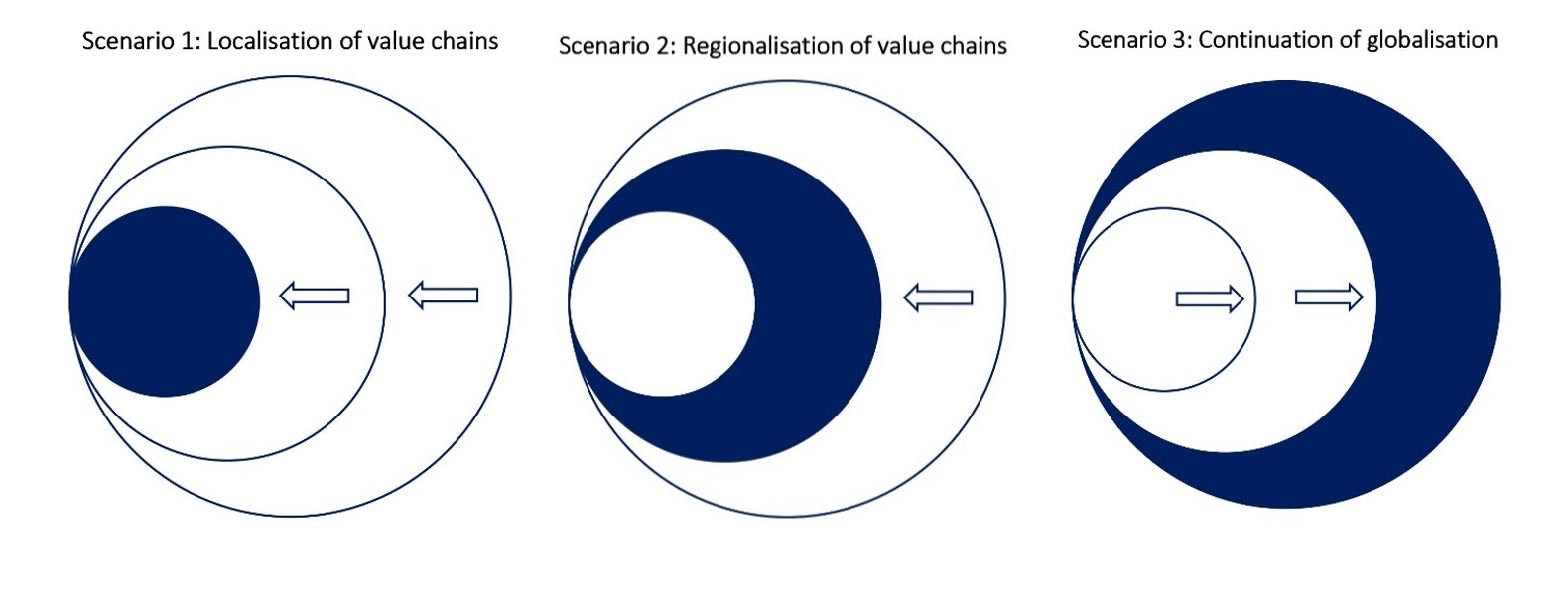

So, what will the impact be on the participation in inter-regional and intra-regional value chains and, ultimately, on economic globalisation? There are at least three scenarios that we can distinguish to analyse the this.

Scenario 1: Localisation instead of globalisation

In this scenario, the pandemic will lead to the collapse of global value chains as national governments adopt protectionist policies and force companies to relocate production facilities closer to home to avoid a reliance on foreign suppliers. The participation of companies in both inter-regional as well as intra-regional value chains will decrease.

The coronavirus outbreak could have a similar negative impact as the 2008 financial crisis

The 2008 financial crisis has already demonstrated that a severe crisis can have a structural negative effect on globalisation. The coronavirus outbreak could have a similar negative impact.

Before the financial crisis, globalisation thrived and GVC value-added production activities grew at a much higher rate than domestic value-added production activities – indicating a strong process of globalisation. However, after the financial crisis the growth of participation in GVCs slowed and did not return to pre-crisis levels.

Between 2012 and 2016, GVC activities as a share of global GDP fell, while the share of domestic production activities rose. Furthermore, the nominal average annual growth rates of complex GVC production activities declined steeply (-1,65%), as did simple GVC production activities (-1,00%) and traditional trade (-0,28%). On the other hand, domestic production activities grew by an average of 1,49% during the same period.

Participation in inter-regional value chains could decrease as the coronavirus outbreak speeds up the process of US-China decoupling. Curtis Chin, Asia fellow at the Milken Institute, warns that COVID-19 will accelerate the process of decoupling more than the trade war as countries and businesses think about their supply chain in the long run.

Participation in intra-regional value chains could also be negatively affected, as might already be the case in the EU. Time Magazine pointed out that “the pillars that were meant to hold up the EU — the free movement of goods and people — crumpled, as borders went back up and panicked governments stockpiled medical supplies with little regard for their neighbours”.

On 25 March, Hungary, for example, banned the commercial export of hydroxychloroquine sulfate, an ingredient used in drugs for coronavirus treatment.

Scenario 2: Regionalisation instead of globalisation

In this second scenario, the pandemic will have a higher impact on complex inter-regional value chains and a lower impact on intra-regional value chains. The coronavirus outbreak will not lead to the end of economic globalisation, rather, it will lead to a strong process of regionalisation.

Philippe Legrain, senior fellow at the London School of Economics, argues that COVID-19 could mark the tipping point that prompts businesses to restructure and shorten their supply chains, “with US companies moving production to Mexico and European ones to Eastern Europe or Turkey”.

The process of regionalisation has arguably already started before the pandemic as the last two decades have seen a spike in new regional trade agreements

The process of regionalisation has arguably already started before the pandemic as the last two decades have seen a spike in new regional trade agreements.

In Europe, the coronavirus outbreak may reinforce the EU’s quest for strategic autonomy and economic sovereignty. These concepts have recently found traction in Brussels as the EU tries to reduce its dependency on third countries – particularly in sectors vital to public health, security and public order.

The pandemic could further reinforce the EU’s ambition for economic sovereignty. On 25 March, European Commission President von der Leyen commented that “as in any crisis, when our industrial and corporate assets can be under stress, we need to protect our security and economic sovereignty.”

Thus, in this second scenario, COVID-19 would permanently change economic globalisation as supply chains shorten and regionalise in response to the pandemic.

Scenario 3: A continuation of globalisation

In the third scenario, economic globalisation will recover once the economic recession has ended and financial markets have recovered from the shock of the coronavirus. Participation in inter-regional GVCs and intra-regional GVCs will recover and economic globalisation will return to pre-corona levels.

Empirical historical data shows that, in the past, the world economy often reacted according to a ‘V-shaped’ model to an epidemic, meaning a quick down and a quick back up. After previous epidemics such as SARS in 2003 and the “Hong Kong” flu in 1968, economic growth fully recovered and more or less absorbed the economic shock.

If globalisation continues, US-China decoupling and COVID-19 will not lead to more regional value chains, but will stimulate companies to shift production to other Asian markets

Contrary to the previous scenario, in this scenario, US-China decoupling and COVID-19 will not lead to more regional value chains, but will instead stimulate companies to shift production to other Asian markets such as Vietnam and Indonesia. As such, global value chains would continue to play an important role.

According to a report from Qima, a Hong Kong-based supply chain inspection company, US buyers already moved their sourcing away from China as inspection demand in China decreased by 14% compared to 2018.

The report states that US companies “were not in a hurry to bring the manufacturing back home, instead dividing the diverted business between near-shoring regions and China’s neighbours in Asia”. Manufacturing, for example, moved to Southeast Asia and Taiwan where inspections and audits from US companies increased by 9.7% in 2019.

Thus, COVID-19 could also trigger a process of diversification of supply chains. Accordingly, global supply chains would be reshuffled, however, not reduced. This means the pandemic would cause individual companies to remodel their supply chains, but accumulatively, RVC and GVC participation could very well return to pre-crisis levels.

Known unknowns and unknown unknowns

As the coronavirus takes hold, the only certainty is that nothing is certain. It is difficult to draw any predictions in the midst of an unfolding event and the degree to which these scenarios play out will be affected by other factors.

There are many known unknowns. How will other developments, such as the digital revolution and the increase in global trade in services, have an impact on global supply chains?

A report on the future of global value chains by the McKinsey Global Institute emphasises that trade in services play a “growing and undervalued” role in global chains. “In 2017, gross trade in services totalled USD 5.1 trillion, a figure dwarfed by the USD 17.3 trillion global goods trade. But, trade in services has grown more than 60 percent faster than goods trade over the past decade.”

There are additionally many unknown unknowns. As said by Winston Churchill: “Never let a good crisis go to waste” - crises can spur the creation of new technologies. Duncan Clark, author of the book ‘Alibaba: the House that Jack Ma Built’, explains how the 2003 SARS epidemic spurred innovation in China’s digital economy.

“The outbreak had a curiously beneficial impact on the Chinese internet sector, including Alibaba. SARS validated digital mobile telephony and the internet, and so came to represent the turning point when the internet emerged as a truly mass medium in China”, Clark writes.

Conclusion

It is still unclear whether global value chains will only be reshuffled, or whether they will be reduced. Whether they will be localised or regionalised, or whether we will see a continuation of globalisation. It could also be the case that we will see a combination of the three scenarios, or an alternative scenario.

The goal of these scenarios is, however, not to predict the future, but to contribute to the debate and enable policymakers and managers to better navigate the uncertainty that COVID-19 will bring about.

It is not important which of the three scenarios will stand the test of time, but whether the supply chain of your organisation would stand the test of these scenarios.

0 Comments

Add new comment