EU-China Investments: Barriers to market access in China

While Chinese investments in Europe are rising, the topic is increasingly becoming more politically sensitive. In October 2018, the Egmont Institute invited several experts to look in detail at the scope, trends and political aspects of Chinese investments in the EU as well as different perceptions of the direct investments across European regions. Is there a unified European strategy towards Chinese investments? And is there a unified Chinese strategy towards the EU? In this Clingendael Spectator series, several of the invited speakers shed their light on EU-China investments. In part I: CEPS Research Fellow Weinian Hu, analyses the main issues still hindering an Investment Agreement.

The EU and China have been negotiating an Investment Agreement (CAI) since 2013. The main issues hindering the conclusion of the Agreement consist of strict barriers to market access in China, Chinese state-owned enterprises’ (SOE) dominant position in the Chinese economy and the nature of Chinese investment in Europe.

Although Chinese foreign direct investment (FDI) in the EU still accounts for around 25 percent of what the EU invests in China, the EU experiences a recent surge of investment by Chinese SOEs in its member states and in the Union’s strategic industries, such as ports, energy infrastructure and the high technology sector. In September 2017, on the grounds of national security or public order, the European Commission proposed an “investment screening instrument”, which would assess foreign investments on the basis of transparency, equal treatment and adequate redress on decisions adopted under review mechanisms. In September 2018, the European Parliament called for “swift adoption” of the instrument. The State of the Union Address delivered by the president of the Commission reiterated transparency and vigilance vis-à-vis foreign investment in the Union. Needless to say, the instrument aims at scrutinising Chinese investment in Europe.

A Chinese SOE can easily outbid a competitor in a merger and acquisition deal in Europe and elsewhere

At this juncture, a legitimate question is why would we complain since these investments could save ailing businesses and industries, generate jobs and increase tax collections. Yet there are three important reasons for being vigilant for Chinese SOEs’ investments in Europe.

Unfair competition

Firstly, Chinese SOEs’ investments may create unfair competition which results in market distortion. Chinese SOEs’ operations are often supported by favourable government policies with convenient access to government funds. Therefore, a Chinese SOE can easily outbid a competitor in a merger & acquisition deal in Europe and elsewhere. This is wholly unfair to genuine market players, since competition will no longer take place among private enterprises, but between private enterprises and China. With a bottomless coffer, a Chinese SOE, but in fact, China, a state, will always defeat private market players, resulting in a distorted market.

If this trend were to continue, Europe’s strategic industries would one day become largely China-owned. It is anybody’s guess what part of these industries would actually remain here.

Secondly, although SOEs exist in many countries, also within the EU, their behaviour is expected to be non-discriminatory vis-à-vis other market players and their conduct should be based on commercial considerations.

Thirdly, there is a major lack of reciprocity between the Chinese and the European FDI regimes. Foreign companies have in principle free access to European markets. By contrast, investment in China is tightly regulated and highly restricted. Markets have a limited role to play, while SOEs’ interests seem paramount in China’s economy.

Drastic SOE reforms

Ever since China’s overall reform started 40 years ago, its SOEs survived drastic reform measures focused on reorganisation, corporatisation and privatisation (stock-exchange listing), which mainly took place in the run-up to China’s WTO accession in the 1990s. It should be noted that these reforms had devastating consequences for the lives of many Chinese citizens. From 1998 to 2003 alone, the SOE workforce was slashed by 35 percent and 40 million SOE employees lost their jobs. Under a planned economy, a SOE functioned as a community providing its employees with all necessary welfare provisions. When a SOE was closed down, its laid-off employees had little social protection to fall back on andcould no longer afford to fall sick.

The reforms seem to have paid off: some SOEs have emerged as the world’s biggest enterprises. 15 Chinese SOEs are among the top 100 enterprises on the Global Fortune 500 List (2017); State Grid ranks second, SINOPEC Group third and China National Petroleum Corporation fourth.

Ultimately, such “easy money”(...) will be detrimental to China’s financial well-being

However, in recent years SOE reform stagnated. Despite the Chinese government’s pledges committed on various occasions since the third Plenum in 2013, barriers to market access still have not been alleviated while preferential policies favouring SOEs persist and SOEs’ easy access to government funds remains. The Chinese government should recommit to the reforms it has undertaken over the past decades.

Barriers to market access

Barriers to market access existing in China are in the form of pre-establishment and post-establishment restrictions. Pre-establishment restrictions come in the form of various government policies limiting the opportunities for FDIs. To begin with, FDIs are classified as either prohibited, restricted, allowed or encouraged under the Catalogue Guiding Foreign Investment in Industry jointly issued by the National Development and Reform Commission (the NDRC) and the Ministry of Commerce (MOFCOM). The classification of a FDI may be adapted over time, on an ad hoc basis, following the baton of the government. This amounts to a structural framework for FDI, with only a minor role for the market to play. To further complicate the situation, government at lower administrative levels may promulgate their respective FDI policies. Additionally, FDI may be admitted on a case-by-case basis. This causes uncertainty, especially to foreign Small and Medium Enterprises (SME), and competition among different governments.

FDI post-establishment restrictions refer to the uneven playing field faced by foreign investors in China in the form of policy restrictions resulting in discriminatory treatment. In contrast, a Chinese investment established in Europe enjoys “national treatment”, a fundamental principle under the WTO multilateral trading system. One hardly hears Chinese investors complaining about discriminatory treatment in Europe.

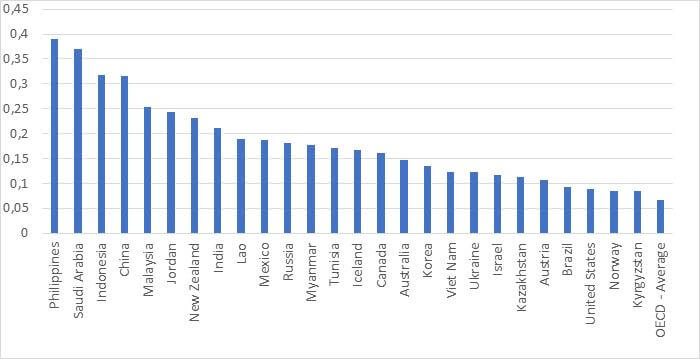

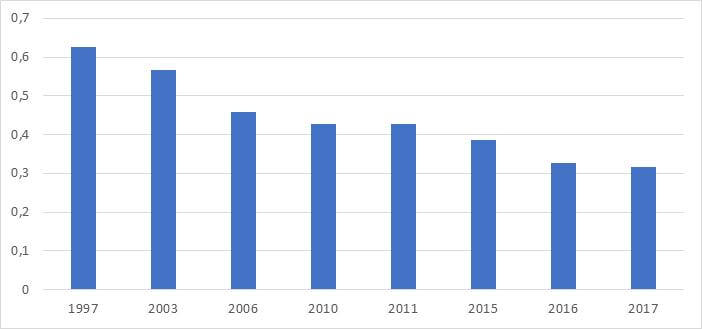

The overall FDI restrictiveness faced by foreign investors in China may be best depicted by the two graphs

In 2017, as in previous years, China was one of the most FDI restrictive countries among 62 countries surveyed by the OECD.

Between 1997 and 2017, FDI restrictiveness in China nearly halved, though changes are minimal in recent years.

Easy money makes for corruption and excessive waste

For SOEs’ easy access to public funds, the “Made in China 2025” strategy provides a striking example. The strategy is a massive manufacturing upgrading programme aiming for technology self-sufficiency in order to substitute and replace the present world leaders (mainly Western and Japanese companies) in terms of market share and technology in ten strategic sectors (amongst which aerospace, railway equipment, numerical control tools and robotics). The financial means that China has committed to the programme is beyond imagination. For example, the Advanced Manufacturing Fund amounts to €2.7 billion and the National Integrated Circuit Fund reaches €19 billion. Additional funds are made available at provincial and municipality level. The majority of beneficiaries of the wealth of financial means can only be SOEs since very few private companies have the capacity in the high technology sectors concerned.

Although appeals for “external pressure” are still heard occasionally, it is not sure if history would repeat itself considering the economic strength and the political prowess of China these days

When massive financial means become available, it engenders a chain of concerns, including oversupply and fraudulence in operation. Ultimately, such “easy money”, jeopardising economic development, will be detrimental to China’s financial well-being.

Similarly, in recent years public finances have entered into equity markets for investing in priority growth sectors and innovation in China. There were 780 state-linked ‘investment funds’ with RMB2.18 trillion (€275 billion) in capital at the end of 2015; and 300 such funds with RMB1.5 trillion (€189 trillion) were established in 2015 alone.

Equally, the huge financial support may result in oversupply which could, in turn, cause excessive waste, as seen by the quick rise and rapid fall of “bike-sharing” in China and in the international markets.

The current SOEs operation model in China also increases vested interest which sets the hurdles for continued reform higher. When the interwoven relationship among governments, financial institutions and SOEs heightens, collusion between bureaucrats and business breeds corruption. Amidst the anti-corruption campaign which has been ongoing since 2012, a number of high-ranking government officials and top executives from SOEs have been charged with corruption. In September 2018, Yao Gang, former vice-chair of the China Securities Regulatory Commission, was sentenced to 18 years and fined EUR1.37 million for insider trading and bribery. On the eve of the Chinese New Year in 2016, it was reported that the president of China National Petroleum Corporation, China’s second biggest SOE and the world’s fourth biggest company (2017), was under corruption probe. His predecessor was sacked on corruption charges too.

External pressure

Certainly, reform must always fight against vested interest in order to succeed. In China’s case, in the past, when the drive for reform appeared weaker than vested interest, “external pressure” was solicited in order for reform to triumph. It worked. In 1979, China and the USA concluded the Agreement on Trade Relations for which China committed to intellectual property rights (IPR) protection. Since IPR legislation did not exist in China at the time at all, both parties agreed to recognise the importance of IPR protection and pledged to provide IPR protection on a reciprocal basis based on laws and international practice. Since then, China has established a comprehensive framework for IPR protection. In a sense, America may have lent a helping hand and exerted “external pressure” so that China resolutely committed to IPR protection as only then technology transfer became possible. One should recall that, after the Cultural Revolution, China was in dire need for the world’s advanced technology to launch its own industrial modernisation strategy.

There is little possibility for agreeing to disagree on the principle of “national treatment”

Although appeals for “external pressure” are still heard occasionally, it is not sure if history would repeat itself considering the economic strength and the political prowess of China these days. The world has become a different place than 40 years ago. Perhaps China would rather proceed at its own pace with its reform agenda.

In the report of the outcomes of the eighteenth round of the EU-China CAI negotiations, it is stated, in addition to fair and equitable treatment, the principle of national treatment as well as its provisions and exceptions still “require further technical follow-up, along the path outlined by the Chief Negotiators”. In the matter of sustainable development, both parties explored options for bridging the gaps in their respective positions.

True enough, for subject matters which fall under sustainable development, such as human rights protection and labour standards, the EU and China have agreed to disagree on the premise of different perceptions, different stages of development, etc. But there is little possibility for agreeing to disagree on the principle of “national treatment” since this is a fundamental rule under the WTO multilateral trading system that both China and the EU have subscribed to.

0 Reacties

Reactie toevoegen